Your Health Insurance Is a Subscription to a System That Doesn't Care If You Live.

Here's What Healthcare Actually Costs When You Leave.

If you are self-employed in the United States and you are under 65, you are paying somewhere between $1,800 and $2,500 a month for health insurance (health, vision, and dental) for a family of four. You know this. You’ve made your peace with it, or you haven’t, but either way, the money leaves the account every month.

In exchange, you have a deductible — probably somewhere between $6,500 and $9,000 per person — which means that the insurance you’re paying for doesn’t actually start paying for much until your family has spent the out-of-pocket. If you have something like Blue Cross, it’s a coinsurance arrangement, and you’re paying while the insurance pays (you usually pay more). This is, by design. You are not a patient to this system. You are a revenue stream.

And let’s say you’re not self-insuring through your own enterprise. Let’s assume you work for someone else. The numbers don’t change; they just burden shift, because whether you realize it or not, you’re paying for all your health care insurance, not your employer. Your employer will pay some percentage, and you will have a percentage deducted from your paycheck. The same screwball system of deductibles and out-of-pocket still applies.

Maybe you’re retired. Well, if you’re like that woman, Sharon Simmons, the “DoorDash Grandma,” that Trump wanted to trot out for “no tax on tips,” then you’re working DoorDash to pay for healthcare (possibly).

It’s really not a pretty picture, regardless.

I want to tell you what healthcare costs could look like when you leave.

Let’s put a real number on the American problem first.

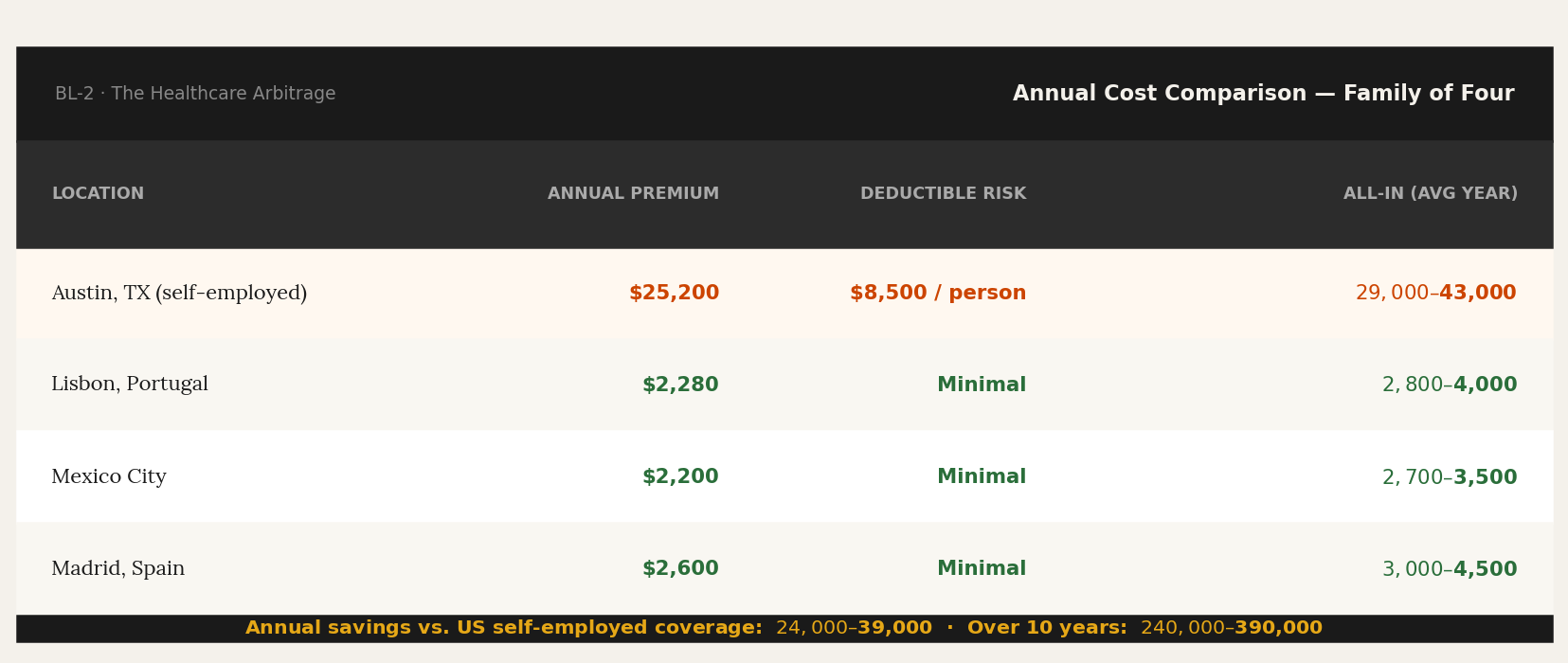

A self-employed couple, both 42, with two kids. ACA marketplace, silver plan, family coverage. In most US metro markets in 2026, premiums are approximately $2,100 per month. Annual premium cost: $25,200. Family deductible before meaningful coverage: $8,500. Out-of-pocket maximum: $18,000.

In a year with any significant medical event — a surgery, a hospitalization, a serious diagnosis — this family can spend $43,200 in premiums and out-of-pocket costs before the insurance actually provides what most people in the rest of the developed world consider “basic coverage.”

In a year without major events, they spend $25,200 plus whatever routine care costs below the deductible.

That is the baseline. Now here’s the comparison.

Portugal.

A private comprehensive family health plan in Portugal — covering GP visits, specialist access, diagnostics, hospitalizations, prescription drugs — runs approximately €150–200 a month for a family of four. Call it €175, or about $190 a month.

There is no meaningful deductible. GP visits have a small copay (€5–15). Specialists charge €30–80 for a private consultation. Emergency care at a private hospital: €100–200 for the visit, more for procedures.

Annual cost: approximately $2,280.

Versus America (Again, continuing from our last article - Austin, Texas): you’re saving $22,920 a year in premiums alone, before accounting for the deductible structure you’ve escaped.

Mexico.

Mexico has a two-track healthcare system. It’s changing, but for now, I’m going to deal with the system was it presently “is” not what it “will be” just yet (but it is getting better, so this story only gets better.) The public system (IMSS) has a voluntary affiliation option for foreigners — an annual cost of approximately $600–700. Private healthcare in Mexico City, Guadalajara, and the major expat hubs is world-class for most conditions and costs a fraction of what it does in the US.

A private supplement plan covering specialist care, hospitalizations, and major procedures: $1,500–2,000 a year.

Total annual healthcare cost for the same family: approximately $2,200–$ 2,700.

GP visit at a private clinic: $25–50. Specialist consultation: $50–100. An MRI, out-of-pocket: $200–$ 400. I have spoken to people who’ve had MRIs in Mexico City and then quietly looked up what the same procedure cost their brother in Houston. The comparison induces a specific kind of rage.

Spain.

Spain’s public healthcare system (SNS) is genuinely excellent and available to legal residents after registration. Private supplemental insurance — which most expats carry for speed and specialist access — runs approximately €150–250 a month for a family.

Annual cost: approximately $1,950–3,250 a year. Spain also maintains some of the best specialized care in Europe — oncology, cardiology, orthopedics — at costs that are simply not comparable to those in the US.

The arithmetic.

The annual savings — relative to US self-employed coverage — range from $24,000 to $39,000 for a typical family. Over ten years: $240,000 to $390,000.

That is not a lifestyle choice.

That is a financial decision.

The objection I hear: “But what about quality? What if something serious happens?”

It’s a fair question that deserves a direct answer rather than reassurance. The honest answer is that for most categories of care — GP visits, specialist consultations, diagnostics, routine procedures, chronic condition management — the quality differential between private healthcare in Lisbon, Mexico City, or Madrid and American healthcare is negligible. The equipment is the same. The training is equivalent.

The wait times are shorter.

For the highest-acuity, most complex cases — certain cancers, rare conditions requiring cutting-edge experimental treatment — US academic medical centers remain among the best in the world. If you have a condition that requires treatment at Johns Hopkins or the Mayo Clinic, that’s a genuine consideration. My suspicion is that if you’re needing treatment from those facilities, you’re either no longer caring about insurance or you’re bankrupt (and either way, I guess you don’t care about insurance). In my own family’s case, both of my in-laws paid considerable expenses for treatment from Mayo and other world-class facilities. It is true that the U.S. has the highest possible quality and range of care. However, it’s going to cost hundreds of thousands of dollars, if not more. We’re talking about a small fragment of the population that needs that level of care, and an even smaller fragment that can afford to engage it without financial ruin.

For the other 97% of healthcare needs a family encounters over a decade, you are not giving anything up. You are getting the same care or better, faster, for a fraction of the cost.

The American healthcare myth — that US quality justifies US prices — is sustained by the people who profit from the pricing, not by the evidence.

Keep reading with a 7-day free trial

Subscribe to Borderless Living to keep reading this post and get 7 days of free access to the full post archives.